The Government of India built a specific solution for exactly this situation — 25 years ago.

It is called CGTMSE. It has enabled over 65 lakh collateral-free loans since 2000. In FY2025 alone, it backed ₹3.05 lakh crore in business loans across India.

Most MSME owners who need it most have never heard of it. This guide changes that.

The Workaround: What Is CGTMSE?

CGTMSE stands for Credit Guarantee Fund Trust for Micro and Small Enterprises.

It was launched on 1 August 2000 — a joint initiative of the Ministry of MSME, Government of India and SIDBI (Small Industries Development Bank of India).

The core idea in one sentence:

You never interact with CGTMSE directly. You approach the bank. The bank handles the guarantee. You get the loan.

How CGTMSE Actually Works — Step by Step

Think of CGTMSE as a silent, government-backed guarantor who never asks you for anything — but gives the bank full confidence to say yes.

Walk into any of the 276 banks and NBFCs registered with CGTMSE — SBI, HDFC Bank, PNB, Bank of Baroda, Canara Bank, ICICI Bank, and hundreds more. Ask specifically for a CGTMSE-backed loan.

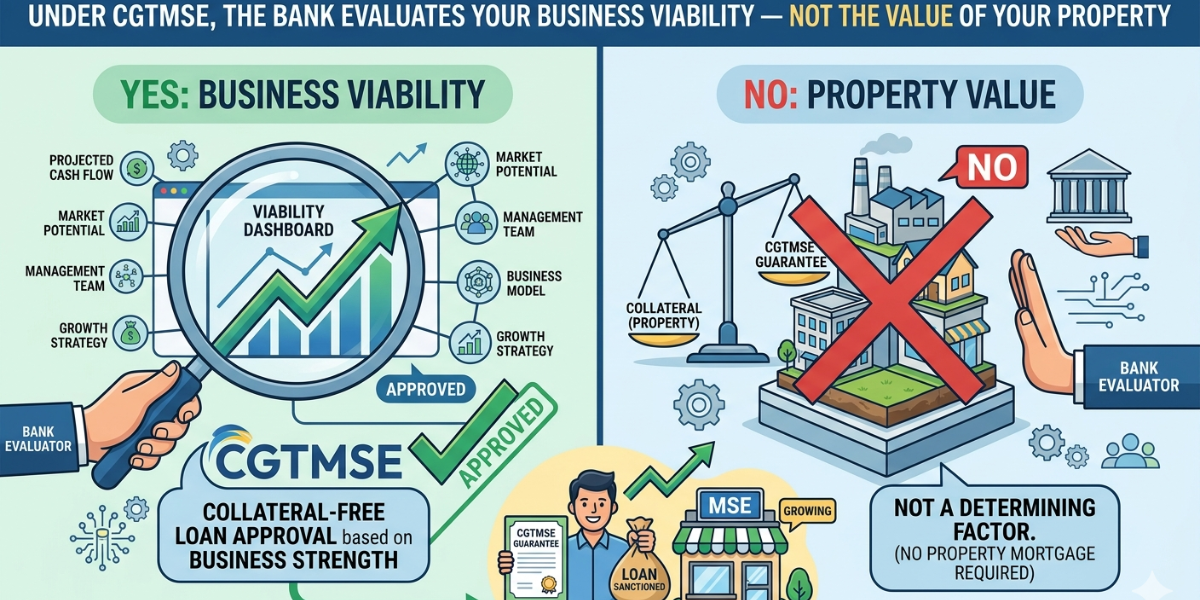

Your first actionThe lender assesses your business viability, cash flow, repayment capacity, project report, and Udyam Registration. No collateral is pledged. The evaluation is entirely merit-based.

Bank’s jobAfter approval, the bank pays an Annual Guarantee Fee (AGF) to CGTMSE to register the loan. This fee is paid by the bank — though some banks factor it into the loan cost.

Behind the scenesThe guarantee runs for the full tenure of the loan. If you repay as agreed, the guarantee is never invoked — it simply exists as a safety net for the bank.

The guaranteeNo land. No building. No gold. No fixed deposit. No personal guarantor. Just your business plan, your Udyam Registration, and your repayment commitment.

You receive the loanHow Much Loan Can You Get Without Collateral?

Union Budget 2025-26, presented by Finance Minister Nirmala Sitharaman on 1 February 2025, doubled the CGTMSE guarantee ceiling from ₹5 crore to ₹10 crore — effective 1 April 2025.

| Loan Type | Maximum Cover | Collateral Needed? |

|---|---|---|

| Term Loan | Up to ₹10 crore | No |

| Working Capital | Up to ₹10 crore | No |

| Composite Loan | Up to ₹10 crore | No |

| Hybrid Security (partial) | Unsecured portion up to ₹10 crore | Partial only |

Who Is Eligible?

✅ You Qualify If You Are

- A new OR existing Micro or Small Enterprise

- In manufacturing, trading, or services

- Registered on Udyam portal (mandatory)

- A proprietorship, partnership, LLP, or Pvt/Public Ltd company

- Assessed as viable by the lender

- Free of any existing bank default or NPA

❌ You Do Not Qualify If

- Your business is in agriculture or allied activities

- You are a Self-Help Group (SHG)

- You run an educational or training institution

- You have an existing NPA with any bank

- Your loan is covered by another govt guarantee

- Your enterprise is a Medium Enterprise

CGTMSE covers only Micro and Small Enterprises — not Medium Enterprises. Under the revised April 2025 classification limits, your enterprise must have investment up to ₹25 crore AND turnover up to ₹100 crore to qualify as Small. Beyond that, you are Medium — and CGTMSE does not apply.

Check your category first: Use our free eligibility calculator →

The One Thing You Must Do Before Approaching Any Bank

Udyam Registration is mandatory for CGTMSE guarantee cover. Without a valid Udyam Registration Number (URN), the bank cannot register your loan with CGTMSE — meaning the collateral-free guarantee cannot be applied, and the bank will ask for collateral by default.

Udyam Registration is completely free and takes 10 minutes at udyamregistration.gov.in.

No Udyam yet? Read: Is Udyam Registration Really Free? Complete Guide 2025 →

Guarantee Coverage — What Percentage Does CGTMSE Cover?

CGTMSE does not guarantee 100% of the loan — it covers a large portion, which is enough for the bank to lend without collateral.

What this means in plain language: If you borrow ₹20 lakh and coverage is 75%, CGTMSE guarantees ₹15 lakh to the bank. If you default, the bank claims ₹15 lakh from CGTMSE. The remaining ₹5 lakh is the bank’s own risk — which is why banks still assess your business carefully. The guarantee removes collateral requirement, not credit scrutiny.

📋 cgtmse.in · SMFG India Credit CGTMSE Guide · Bankopedia CGTMSE Guide (2026)The Hidden Option — Hybrid Security Model

You do not have to choose between full collateral and no collateral. Under the Hybrid Security model — you pledge whatever partial collateral you have, and CGTMSE covers the unsecured remainder up to ₹10 crore.

Example: You need ₹30 lakh. You own equipment worth ₹8 lakh.

Total loan = ₹30 lakh. Total additional collateral needed = ₹0.

Annual Guarantee Fee — What Does It Cost?

There is an Annual Guarantee Fee (AGF) charged to the lending institution — not directly to you. The bank pays CGTMSE. Many banks factor this into the loan cost. Effective 1 April 2025:

| Loan Amount | Annual Guarantee Fee | Who Pays |

|---|---|---|

| Up to ₹10 lakh | 0.37% per annum | Bank (may pass on) |

| ₹10 lakh – ₹1 crore | Graduated rates | Bank (may pass on) |

| ₹8 crore – ₹10 crore | 1.20% per annum | Bank (may pass on) |

ZED Certified units get a 10% discount on the applicable fee. Units in notified regions also get concessions.

📋 blog.jumpp.finance CGTMSE Fee Guide · cgtmse.in Scheme Document (effective 1 April 2025)Documents Required — What to Carry to the Bank

- Udyam Registration Certificate — mandatory, non-negotiable

- KYC documents — Aadhaar, PAN of proprietor / partners / directors

- Business registration proof — incorporation certificate, partnership deed, etc.

- Bank statements — last 6–12 months

- Income Tax Returns — last 2–3 years (if filed)

- GST Returns — if GST registered

- Project report / business plan — especially critical for new businesses and large amounts

A well-prepared project report is the single biggest factor under CGTMSE. The guarantee removes collateral risk for the bank — but not credit risk. The bank still needs to believe your business is viable. Spend real time on your project report. Ask the bank’s MSME desk for their standard template.

CGTMSE vs Regular MSME Loan — Key Differences

| Feature | Regular MSME Loan | CGTMSE Loan |

|---|---|---|

| Collateral required | Usually yes | No |

| Third-party guarantor | Often required | Not required |

| Maximum loan | Depends on collateral | Up to ₹10 crore |

| Government backing | None | 75%–85% guarantee |

| Udyam Registration needed | Recommended | Mandatory |

| Best for | Asset-rich businesses | First-gen entrepreneurs, asset-light MSMEs |

Which Banks Offer CGTMSE Loans?

CGTMSE has 276 Member Lending Institutions (MLIs) — walk into almost any major bank and ask for a CGTMSE-backed MSME loan:

- All major Public Sector Banks — SBI, Bank of Baroda, Punjab National Bank, Canara Bank, Union Bank, Indian Bank

- Major Private Sector Banks — HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra Bank

- Regional Rural Banks (RRBs) — for rural and semi-urban MSMEs

- Select Urban Co-operative Banks

- Select NBFCs registered as MLIs with CGTMSE

What Cannot Be Financed Under CGTMSE?

- Loans already covered by DICGC or RBI guarantee schemes

- Loans to Self-Help Groups (SHGs)

- Loans for agriculture, fisheries, and livestock

- Loans for educational and training institutions

- Loans sanctioned fully against existing collateral

- Consumer or non-business purpose loans

- Loans to Medium Enterprises

Frequently Asked Questions

No. CGTMSE does not give loans to borrowers directly. You must approach a bank or NBFC that is a registered MLI. The bank applies for the CGTMSE guarantee cover on your behalf after approving your loan.

No. Existing personal loans do not affect your CGTMSE eligibility. However, if you have any business loan classified as NPA with any bank, you are not eligible for CGTMSE coverage on a new facility.

The bank must assess your business as viable and profitable with a good track record. For new enterprises, viability is judged on the business plan and projected cash flows. The guarantee removes collateral requirement — not credit assessment.

No. CGTMSE covers only Micro and Small Enterprises. Medium Enterprises are excluded. Check your classification against the revised April 2025 limits before applying.

Ask your bank to share the Credit Guarantee Number (CGN) issued by CGTMSE upon registration. This is your written confirmation that the guarantee cover is active on your loan.

Do not give up. Each bank has different internal credit policies. Check your CIBIL score (free once a year at cibil.com) for errors. Consider the Udyam Mitra portal (udyammitra.in) — a government platform that connects MSMEs with lenders under CGTMSE. Also approach select NBFCs registered as MLIs, which often have more flexible assessment criteria.

This article is for informational purposes only. Loan approval is subject to individual lender assessment. For official scheme details, visit cgtmse.in.